Monthly Foreign Exchange Review

Our latest Foreign Exchange Outlook explores how declining energy prices, resilient U.S. economic data, shifting rate policies and ongoing geopolitical risks are shaping currency markets. While the dollar remains firm for now, the outlook into July and beyond could change quickly if lower oil prices begin flowing toward inflation.

Oil prices collapsed below $70/barrel, pointing to an end of the Iran event, and calming global markets. Still, gasoline prices remain stubbornly elevated at $4.08—implying $95/barrel oil. This is the largest gasoline-to-oil price difference in at least the last 10 years. Strait of Hormuz traffic has recovered to only 20% of pre-war volume after 16 days. Meanwhile, China has effectively withdrawn from global energy markets, removing 6m barrels of demand. This must return at some point. Markets have thankfully calmed, but we remain in dangerous territory. A major energy price disruption unfortunately remains a real risk. Current path is for oil to stabilize in the $70/barrel range, which would be a boost to the U.S. and world economy.

U.S. inflation remains hot, though June data does not reflect the recent drop in oil prices. CPI rose 4.2% year-over-year in May, up sharply from 3.8% in April, while Core CPI came in at 2.9%. PPI added to concerns, printing 1.1% month-over-month! The recent collapse in oil prices has not yet flowed through to consumer prices or the data, but inflation remains a dominant concern for markets and policymakers.

The labor market showed surprising strength in May numbers, beating expectations by a wide margin. May nonfarm payrolls came in at 172k against an 88k survey, with April revised up to 179k. This is solid job growth. The labor market continues to run warmer than many expected given the macro backdrop.

The U.S. economy showed more resilience than expected in June. Q1 GDP was revised up to 2.1% from the prior 1.6% estimate. ISM Manufacturing hit 54, retail sales beat at +0.9%, and the University of Michigan sentiment index recovered from 44.8 to 49.5—still historically low but moving in the right direction. Durable goods reversed sharply in May to -4.5% after April's exceptional 8.5% print, a soft spot in an otherwise stronger data month. The U.S. economy seems to be moving to solid or even strong growth after a slow Q1.

The USD strengthened 2% against the index as oil prices fell. The dollar benefited from its safe-haven status and the relative strength of the U.S. economy versus energy-importing peers. EUR fell to the bottom of its one-year channel, CAD broke out to 1.4200, and JPY weakened to its lowest level against the dollar since 1986.

Rate expectations have shifted toward hikes, while long-end rates have paradoxically fallen. The Fed held rates steady at 3.75% at the June 17 FOMC meeting. Markets are now pricing 1.5 hikes over the next 12 months. New Fed Chair Warsh signaled reduced forward guidance going forward—a meaningful policy communication shift. The 10-year Treasury yield has dropped 35 basis points since May 15, suggesting the bond market sees the oil collapse as ultimately disinflationary, even as near-term CPI data remains hot.

July Outlook: USD firm, with a major wildcard in the oil-to-gas price lag. If pump prices follow oil lower, inflation expectations could shift rapidly, which would reprice rate expectations and weaken the USD. Until that happens, the USD carries structural support. Energy volatility remains the dominant risk, and any resumption of Strait traffic or Chinese re-entry into energy markets could move prices sharply.

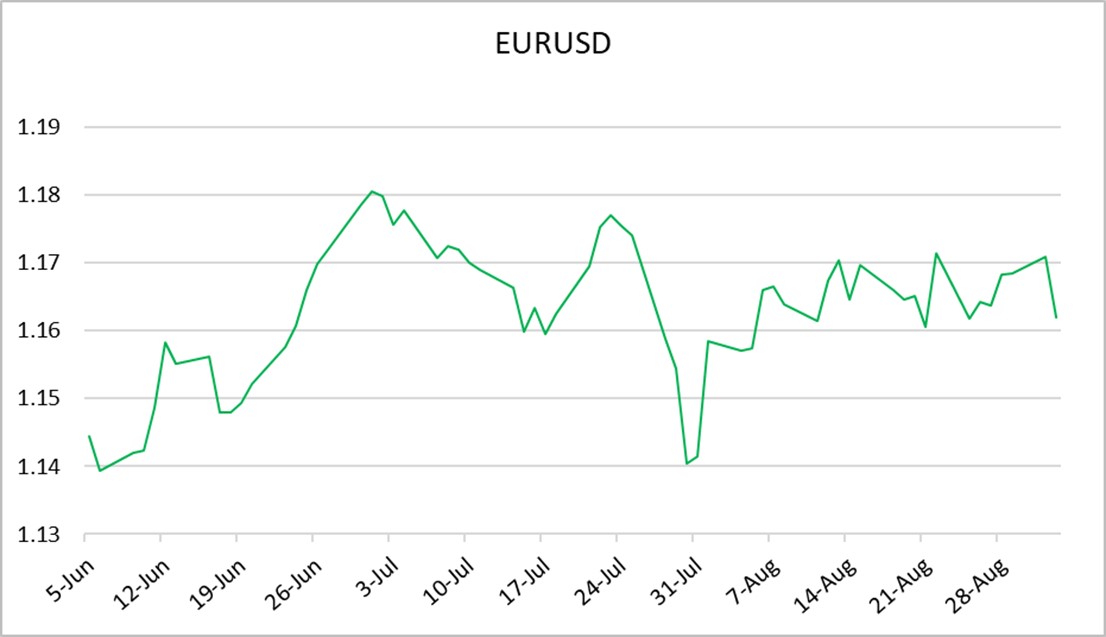

EUR/USD

Source: Bloomberg Finance LP

June was a significant month for the euro. The ECB hiked 25bps on June 11, its first increase since 2023, citing inflation forecast at 3.0% for 2026. The counter-argument: falling oil prices post a U.S.-Iran peace deal are pulling inflation expectations lower. EURUSD hit a one-year low near 1.1320 mid-month before recovering to 1.1420. Watch the July 24 ECB meeting—another hike would be a genuine surprise The Fed-ECB rate differential remains the dominant headwind for this pair.

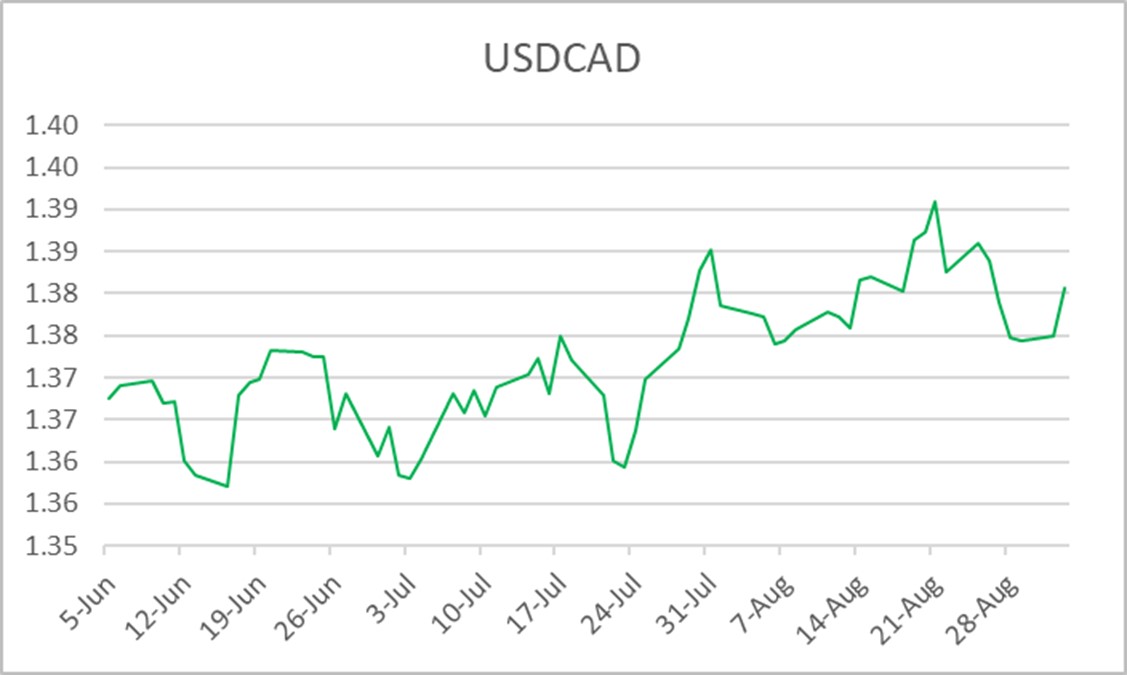

USD/CAD

Source: Bloomberg Finance LP

CAD was pressured nearly every day in June. Canada's Q1 GDP confirmed a second consecutive quarter of mild contraction, and the full-year 2026 growth forecast has been slashed to 0.7%. The BoC held at 2.25% and described the policy outlook as a genuine “dilemma”: weak growth argues for cuts, CPI at 3.2% argues for hikes. A blowout May jobs report (+87,800) was the one bright spot.

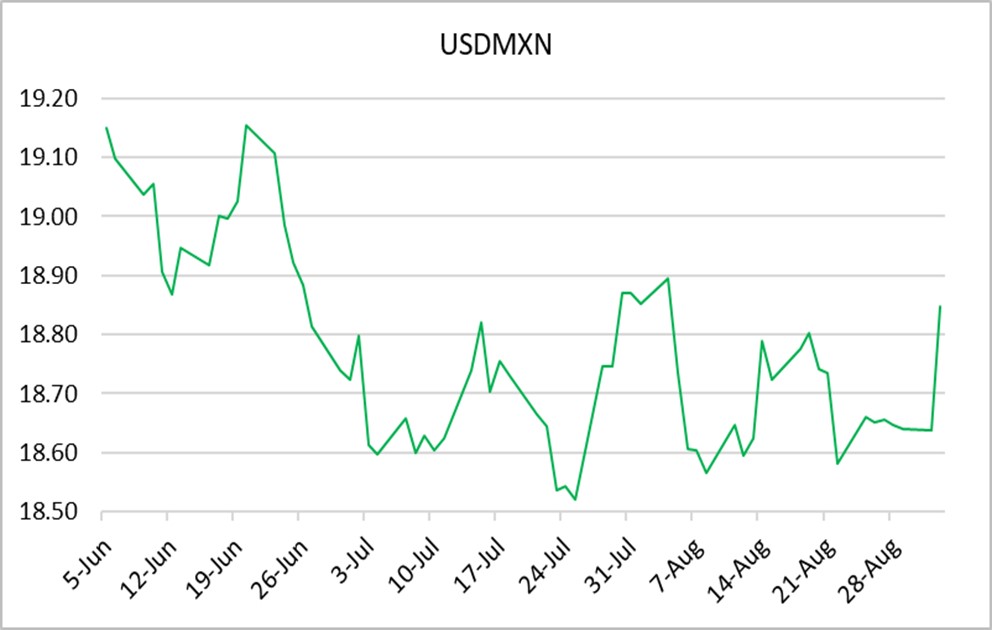

USD/MXN

Source: Bloomberg Finance LP

The MXN carry trade is losing some of its shine. Banxico held at 6.50% on June 25, formally ending its two-year easing cycle. Inflation surprised to the downside at 3.5% in early June, and the 2026 GDP forecast was trimmed to 1.1%. USDMXN bounced again off the 17.10 level; this has been support since January 26. No Banxico meeting in July.

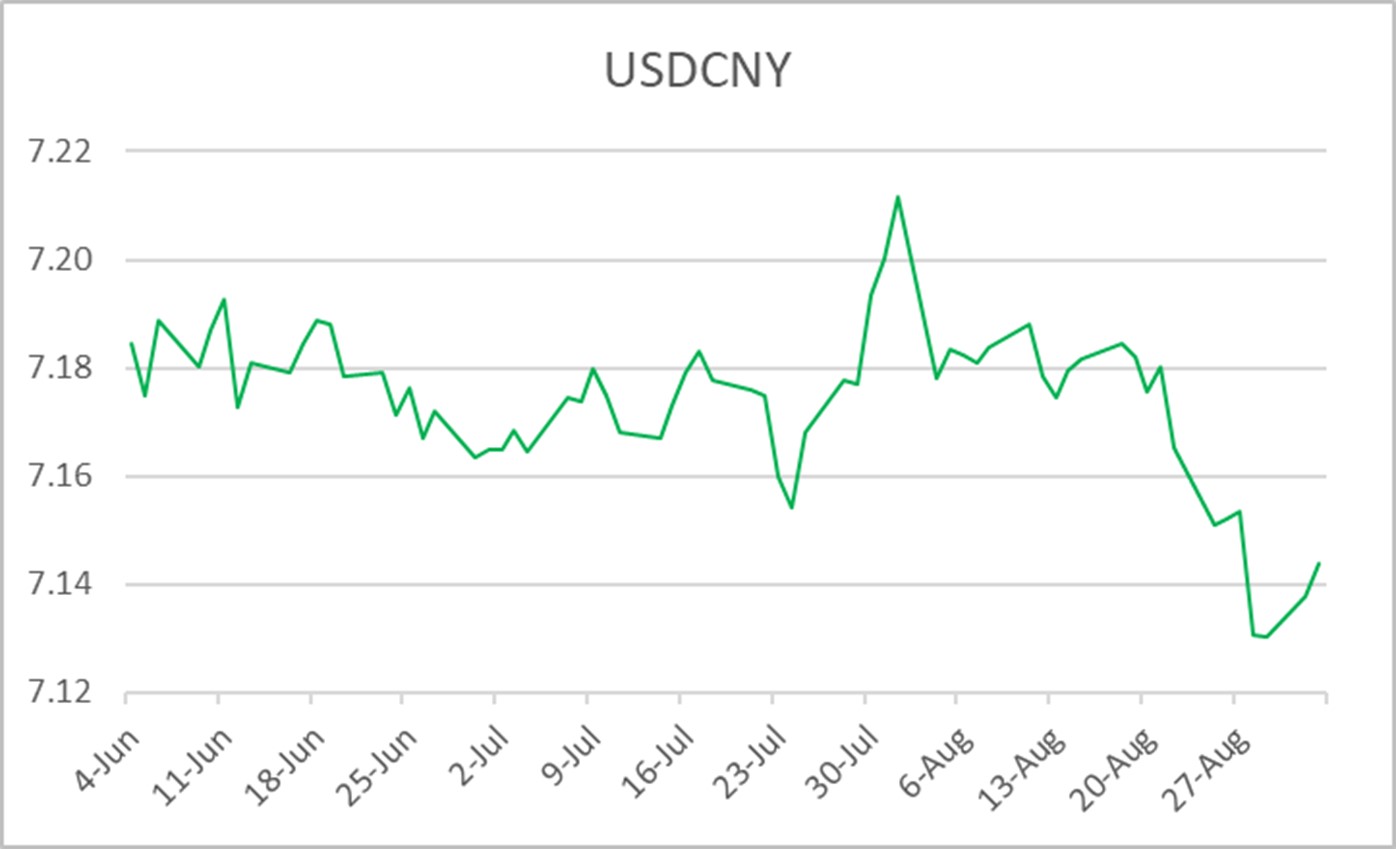

USD/CNY

Source: Bloomberg Finance LP

USDCNY is being pulled in two directions. China's exports surged 19% YoY in May, and the yuan had been on a strengthening trend for much of 2026. But the Fed's hawkish turn in June reversed that trend. The PBOC set its fixing above market estimates on multiple days, signaling comfort with a modestly weaker yuan. Bipartisan U.S. senators are pressing Treasury Secretary Bessent to push China on currency undervaluation at the G7. The big picture: this pair is moving on trade headlines more than data.

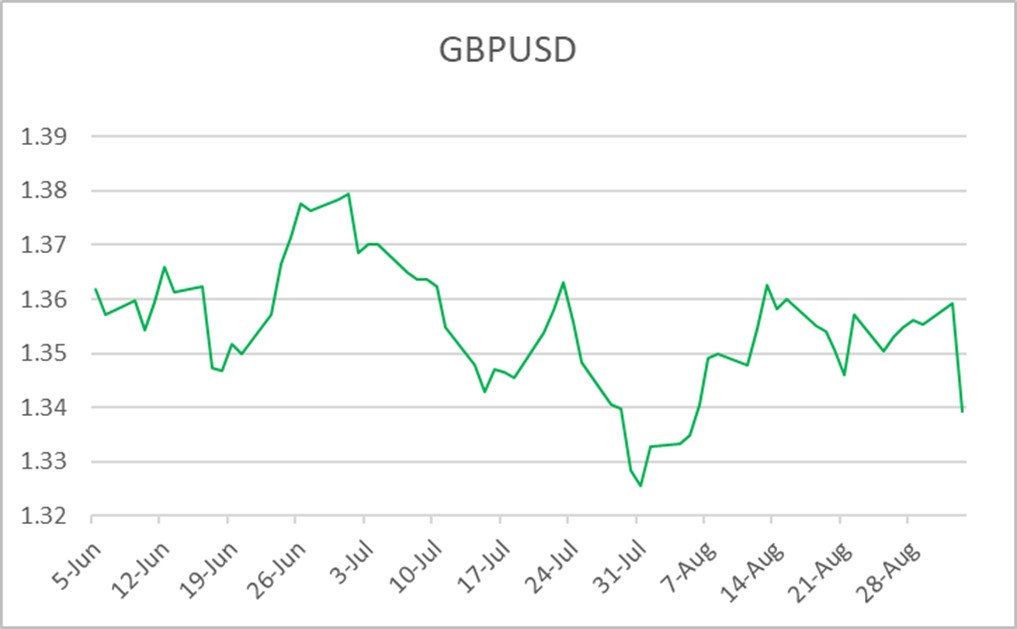

GBP/USD

Source: Bloomberg Finance LP

GBPUSD hit a seven-month low of 1.3156 on June 24 before recovering to 1.3260. The BoE held at 3.75% on June 18 in a 7-2 vote. PM Starmer resigned following local election losses; Andy Burnham takes over and pledged fiscal discipline. PMI slipped to 49.4 in June, while GDP grew a measly 0.6%. Goldman Sachs flagged GBP as the most overvalued G10 currency. Brexit “celebrated” its 10-year anniversary in June—yet it undeniably has made the UK economy weaker and less resilient, and slowed growth.

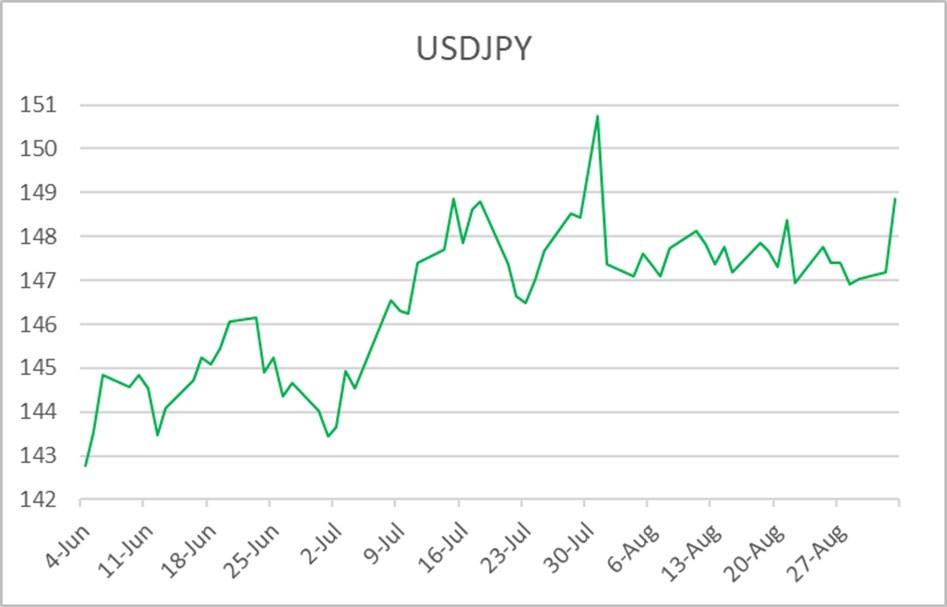

USD/JPY

Source: Bloomberg Finance LP

USDJPY broke through 162 the last day of June. This is a 40-year high for the dollar against the yen despite the BoJ hiking to 1.0%--the highest rate since 1995. The divergence between a hiking BoJ and a hold-steady Fed has not been enough to arrest yen weakness. Japanese authorities confirmed no intervention between May 28 and June 26, and strategists now watch 163 as the next threshold.

Associated Bank can transact foreign exchanges in more than 100 currencies. Companies interested in learning more about making payments in foreign currencies or in hedging currency exposures should contact their Associated Bank Relationship Banker or the bank’s Corporate Foreign Exchange Department at 866-524-8836 or email fxcapmarkets@associatedbank.com.

All rates shown are indications only and subject to change. Foreign exchange contracts are subject to foreign currency exchange risk and are NOT deposits or obligations of, insured or guaranteed by Associated Bank, N.A. or any bank or affiliate, are NOT insured by the FDIC or any agency of the United States, and involve INVESTMENT RISK, including POSSIBLE LOSS OF VALUE. This material is provided to you for informational purposes only; and any use for other than informational purposes is disclaimed. It is a summary and does not purport to set forth all applicable terms or issues. It is not intended as an offer or solicitation for the purchase or sale of any financial product and is not a commitment by Associated Banc-Corp, its subsidiaries or affiliates, as to the availability of any such product at any time. The information herein is not intended to constitute legal, tax, accounting, or investment advice, and you should consult your own advisors as to such matters and the suitability of any transaction. We make no representations as to such matters or any other effects of any transaction. In no event shall we be liable for any use of, for any decision made or action taken in reliance upon, or for any inaccuracies or errors in, or omissions from, the information herein. The views expressed here are solely those of the author and do not reflect the views of Associated Banc-Corp, its subsidiaries or affiliates.