Monthly Interest Rate Update

Interest rates have surged to 16-month highs, driven by persistent inflation, increased global debt issuance and the massive AI infrastructure buildout. Despite a consensus for steady economic growth and modest rate changes, ongoing uncertainty and volatility mean risk management remains crucial.

Treasury yields have been on quite a ride lately. They hit their highest levels in sixteen months as investors finally let go of the idea that the Fed might cut rates anytime soon. The shorter end of the curve moved the most with the 2‑year and 5‑year yields jumping about 66 basis points from February to mid‑May, and the 10‑year climbing about 50. We’ve seen a bit of relief since then, with the 10‑year drifting down about 20 basis points over the past couple of weeks, but the curve has still flattened by roughly 6 basis points since February.

What’s driving all this isn’t exactly new. The conflict—and now the tentative ceasefire—in the Middle East has kept oil prices elevated, and those higher energy costs are starting to show up in broader inflation data. Add in the lingering impact of last year’s tariffs, and price pressures just aren’t letting up. CPI hit 3.8% last month, the highest in three years, and Core PCE reached 3.3%, a level we haven’t seen in nearly two years. Inflation has now been above the Fed’s 2% target for five straight years. That puts the new Fed Chair, Kevin Warsh, in a tough spot if he wants to make a case for easier policy.

Another factor pushing rates higher is the sheer amount of long‑term debt hitting the market. The U.S. is issuing heavily—partly to cover costs tied to the Middle East—but it’s not just the U.S. Countries across Europe, along with Canada, Australia, Japan and South Korea, have all boosted defense spending by 15-25% as the U.S. steps back from its traditional security role. With debt‑to‑GDP ratios already above 100% in the U.S., near 200% in Japan and closing in on 90% in the Euro area, investors have a lot of government paper to absorb.

And then there’s the AI buildout. The infrastructure behind it is expected to cost more than $3 trillion. Big tech firms —the hyperscalers—have already issued approximately $500 billion in long‑term bonds across 2025 and 2026. That wave of corporate issuance is starting to nudge borrowing costs higher and will likely keep some upward pressure on long‑term rates. Thirty‑year Treasury yields are hovering near 5%, a level we haven’t seen since 2007.

Looking ahead, futures markets are pricing in just one quarter‑point Fed rate hike by January 2027, with not much else happening after that. Bloomberg’s monthly survey of economists is a bit more dovish, even though inflation is expected to stay above 3% into 2027. The consensus outlook is pretty calm: slow but positive GDP growth, no recession, modest job creation, unemployment holding in the mid‑4% range and a gentle drift lower in both short‑ and long‑term rates.

But when you think about what we’ve lived through over the past six years: a pandemic, inflation peaking at 9%, massive rate hikes followed by cuts, sweeping tariff changes, a major regional war and the rollout of a transformative new technology—the consensus feels a little too relaxed. Median forecasts tend to smooth out the real uncertainty underneath. The economy is sturdy, but it’s not predictable.

That’s why our advice hasn’t changed: plan for surprises. In addition to your normal business risk management practices, your Associated Bank banker can help you use the financial tools available, including interest rate and FX hedging, to protect your business from the kinds of shocks that don’t show up in a median forecast.

Key Statistics: Interest Rates, Unemployment and Inflation

| Year-end 2022 | Year-end 2023 | Year-end 2024 | Year-end 2025 | May 29, 2026 | |

|---|---|---|---|---|---|

| 10-yr Treasury yield | 3.87% | 3.88% | 4.57% | 4.17% | 4.44% |

| 2-yr Treasury yield | 4.43% | 4.25% | 4.24% | 3.47% | 4.00% |

| Spread | -0.56% | -0.37% | 0.33% | 0.70% | 0.44% |

| Fed Funds Target (mid) | 4.375% | 5.375% | 4.375% | 3.625% | 3.625% |

| CME Term SOFR 1-mo | 4.36% | 5.35% | 4.33% | 3.69% | 3.62% |

| CPI (y/y change) | 6.5% | 3.1% | 2.7% | 2.7% | 3.8% |

| Core PCE (monthly) | 4.7% | 3.16% | 2.81% | 2.83% | 3.3% |

| 5-yr TIPS (market breakeven) | 2.38% | 2.15% | 2.39% | 2.27% | 2.54% |

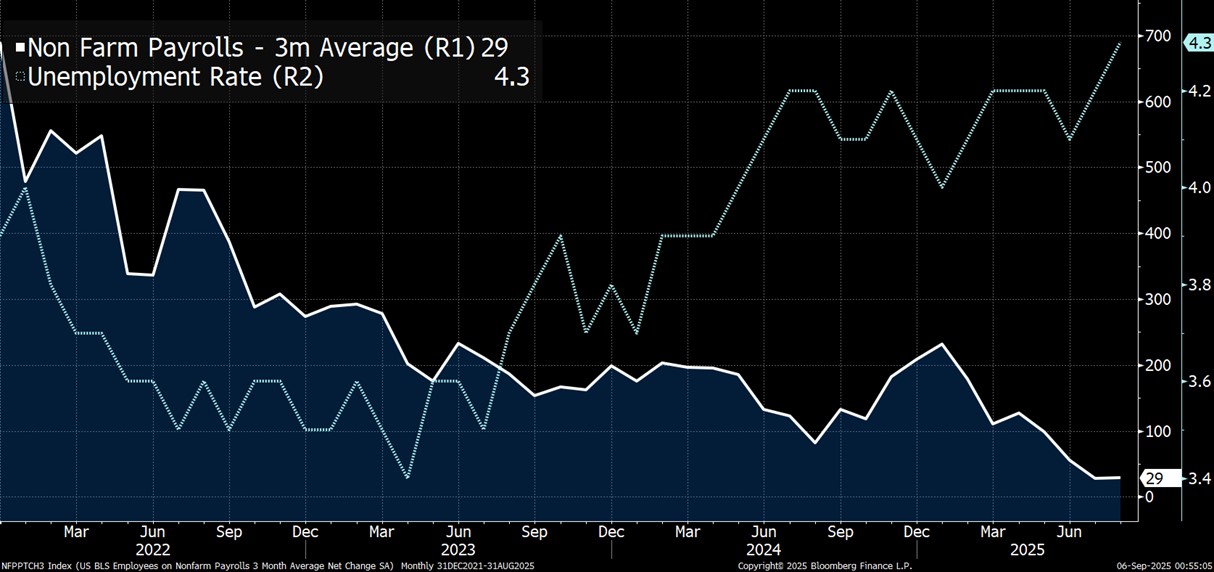

| U-3 Unemployment | 3.5% | 3.7% | 4.1% | 4.4% | 4.3% |

| Real avg weekly earnings | -3.1% | 0.5% | 1.0% | 1.1% | 0.2% |

| Annual change in NFP jobs | +4,503,000 | +2,560,000 | +1,450,000 | +371,000 | +158,740 |

Benchmark Interest Rates – LT

Source: Bloomberg Finance LP

-

The 1-month SOFR floating rate benchmark has drifted down 6 bp this year, tracking the Fed funds target. Meanwhile, 2-year and 5-year Treasury yields have backed off their 15-month peak.

-

Two-year Treasuries, in particular, are up 66 bp from their February lows.

Bloomberg Survey of 88 Economists

May 15-20, 2026

Source: Bloomberg Finance LP

Associated Bank offers a wide range of instruments for hedging interest rate, commodity and foreign currency risk, including foreign exchange in more than 75 currencies. Companies interested in learning more about these instruments should contact their Associated Bank Relationship Banker or the bank’s Capital Markets Department at 866-524-8836.

All rates shown are indications only and subject to change.

This material is provided to you for informational purposes only; and any use for other than informational purposes is disclaimed. It is a summary and does not purport to set forth all applicable terms or issues. It is not intended as an offer or solicitation for the purchase or sale of any financial product and is not a commitment by Associated Banc-Corp, its subsidiaries or affiliates, as to the availability of any such product at any time. The information herein is not intended to constitute legal, tax, accounting, or investment advice, and you should consult your own advisors as to such matters and the suitability of any transaction. We make no representations as to such matters or any other effects of any transaction. In no event shall we be liable for any use of, for any decision made or action taken in reliance upon, or for any inaccuracies or errors in, or omissions from, the information herein. The views expressed here are solely those of the author and do not reflect the views of Associated Banc-Corp, its subsidiaries or affiliates.