Quarterly Economic and Market Review

Our quarterly market review covers the oil price shock, Fed uncertainty, and new tariff rulings. First quarter’s defining event was the late-February escalation in the Middle East, where U.S. and Israeli strikes on Iran triggered prolonged tensions. The fallout: surging energy prices, rising volatility, and broad declines across global equity and fixed income markets.

- Oil Price Shock-2026 began with strong growth in most markets until war with Iran led to spiking energy costs, steep equity market losses and rising bond yields.

- Fed Uncertainty Inside and Out-Kevin Warsh is the nominee to succeed as Federal Reserve Chairman, but politics complicate his confirmation and inflation risks have changed interest rate expectations this year.

- Tarrifs Out, Tarrifs In-The Supreme Court deemed most tariffs enacted in 2026 were illegal, but new tariffs were quickly implemented to leave the effective tarrif rate mostly unchanged-for now.

The War in Iran and the price of oil

A critical factor has been the disruption of the Strait of Hormuz*, a narrow waterway off Iran’s coast through which more than 20% of the world’s oil supply passes daily. Since the onset of the conflict, Iran has effectively halted traffic through the Strait, stranding tankers and severely disrupting regional energy supply chains.

Oil markets reacted swiftly. Brent crude rose from approximately $70 per barrel in February to over $115 on March 9, before retreating below $90 later that same day. Prices have remained volatile within this range, though some projections suggest oil could reach $180–$200 per barrel if the disruption persists. Even in the event of a near-term resolution, damaged infrastructure is likely to delay a full recovery in production capacity.

The broader economic implications remain uncertain. As of late March, U.S. gasoline prices reached an average of $4 per gallon—the highest level since 2022. Elevated energy costs risk pushing inflation higher; the Federal Reserve estimates that a 10% increase in oil prices may add approximately 0.3% to consumer price inflation. Sustained price pressure could also constrain discretionary spending. However, the U.S. economy remains relatively well-positioned compared to global peers, supported by strong domestic energy production and underlying resilience. Current estimates still point to modest positive GDP growth of approximately 1–2% for the first quarter.

Capital Markets Shift from Confidence to Caution

Market performance in the first quarter unfolded in two distinct phases. Early in the year, smaller capitalization U.S. equities and international markets outperformed large-cap U.S. stocks, continuing the broadening participation from last year. In contrast, the software sector lagged, as the release of a new AI model from Anthropic and related research raised concerns about long-term disruption to traditional software business models. Many private-credit firms, especially those with heavy software exposure, were also swept up, with several funds seeing redemption pressures and limiting withdrawals.

As capital rotated away from software, previously underperforming areas began to recover. Smaller U.S. companies benefited from expectations of lower interest rates and easing tariff pressures, while international equities were supported by a weakening U.S. dollar and reduced trade frictions.

This constructive backdrop shifted abruptly in late February as geopolitical tensions escalated into open conflict. Major equity indices quickly entered correction territory, declining more than 10% from their January highs.

The change in market leadership was equally pronounced. Early quarter strength in growth oriented sectors reflected a “risk on” environment characterized by strong investor sentiment and low volatility. That dynamic reversed as the quarter progressed. Cyclical sectors came under pressure, while defensive sectors and commodities outperformed. Energy equities saw significant inflows, while investor positioning shifted away from higher-risk growth exposures. A more cautious, “risk-off” stance became dominant.

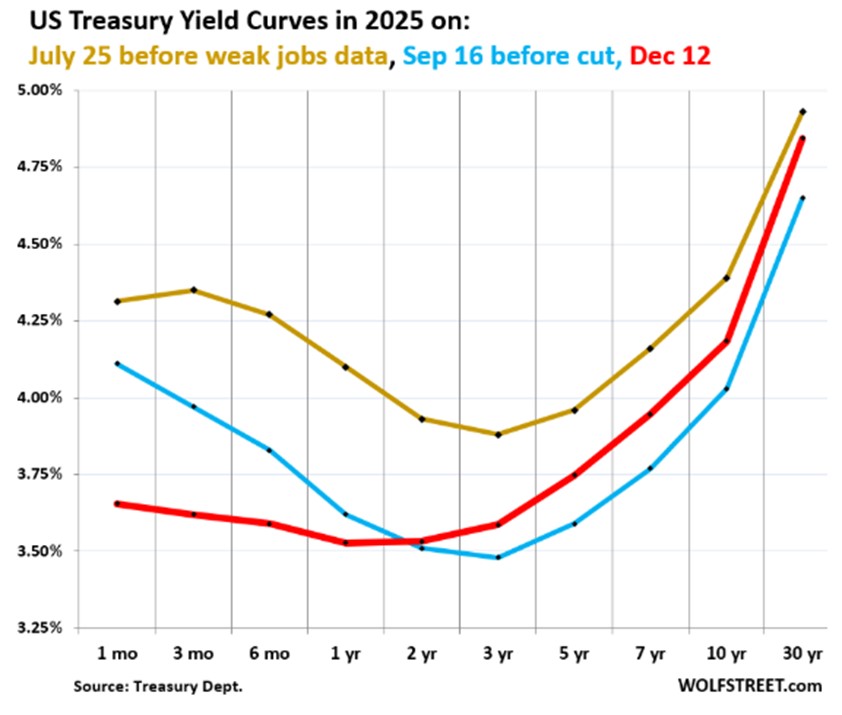

Fixed income markets reflected similar concerns. Treasury yields moved higher as investors priced in both the inflationary impact of elevated energy prices and a more uncertain monetary policy outlook. The yield on the 10-year U.S. Treasury reached 4.44% in late March. Credit spreads, which had been historically tight, widened modestly, indicating a rise in overall risk aversion.

Federal Reserve Pressures

Expectations for monetary policy shifted materially over the course of the quarter. Prior to the escalation in geopolitical tensions, the Federal Reserve was widely expected to continue cutting interest rates through 2026. By the end of March, however, market expectations had adjusted toward an extended pause, with some limited speculation around potential rate increases.

Rising energy prices have complicated the Fed’s policy outlook. Inflation remains above target, while labor market momentum has slowed, creating a challenging environment for policymakers attempting to balance price stability and economic growth.

Leadership uncertainty has added another layer of complexity. With Chairman Jerome Powell’s term set to expire in May, attention has turned to his potential successor. In January, President Trump nominated Kevin Warsh, a former Federal Reserve governor, to assume the role. While initially viewed as a likely confirmation, the process has become less certain amid increasing political tension surrounding the Fed.

This tension has been driven in part by efforts to remove Governor Lisa Cook and a Department of Justice investigation into Chairman Powell related to testimony on the Federal Reserve’s headquarters project. Although a federal judge dismissed the DOJ’s attempt to issue subpoenas in March, the decision was quickly appealed.

The continuation of this legal challenge has introduced political friction, particularly within the Senate Banking Committee. Republican Senator Tom Tillis of North Carolina, a key vote in the confirmation process, has indicated that the ongoing case could delay consideration of Warsh’s nomination. As a result, both the timing and direction of future Fed leadership remain uncertain.

Trade Policy Back in Focus

Trade policy re-emerged as a central theme during the quarter. On February 20, the Supreme Court ruled that the International Emergency Economic Powers Act (IEEPA) does not grant the president authority to impose tariffs, reaffirming that taxation powers reside with Congress. While not all tariffs implemented were struck down, this decision invalidated tariffs specifically implemented under IEEPA authority and raised questions regarding the disposition of approximately $142 billion in revenue collected during 2025.

The ruling introduces significant uncertainty. Key questions remain unresolved, including whether refunds will be issued and to whom. Prior to the decision, the effective U.S. tariff rate had risen to approximately 10.3% in January 2026, up from 2.3% one year earlier. This increase had already contributed to shifts in trade flows, purchasing behavior and pricing, particularly in industries sensitive to global supply chains such as autos, capital goods, and semiconductors.

Despite the ruling, trade policy remains fluid. Shortly after the decision, the administration introduced a temporary 10% baseline tariff under Section 122 of the Trade Act of 1974. Additional proposals to raise tariffs to as high as 15% on certain trading partners have also been discussed, though any changes remain subject to further regulatory and congressional review.

This evolving policy landscape continues to create uncertainty for both producers and consumers. When combined with elevated energy prices, the risk of renewed inflationary pressure has increased. Even incremental policy adjustments, layered onto an already complex macroeconomic environment, have the potential to meaningfully influence economic outcomes.

Investment, Securities and Insurance Products:

NOT

FDIC INSUREDNOT BANK

GUARANTEEDMAY

LOSE VALUENOT INSURED BY ANY

FEDERAL AGENCYNOT A

DEPOSITAssociated Bank and Associated Bank Private Wealth are marketing names Associated Banc-Corp (AB-C) uses for products and services offered by its affiliates. Securities and investment advisory services are offered by Associated Investment Services, Inc. (AIS), member FINRA/SIPC; insurance products are offered by licensed agents of AIS; deposit and loan products and services are offered through Associated Bank, N.A. (ABNA); investment management, fiduciary, administrative and planning services are offered through Associated Trust Company, N.A. (ATC); and Kellogg Asset Management, LLC® (KAM) provides investment management services to AB-C affiliates. AIS, ABNA, ATC, and KAM are all direct or indirect, wholly-owned subsidiaries of AB-C. AB-C and its affiliates do not provide tax, legal or accounting advice. Please consult with your advisors regarding your individual situation. (1024)

Readers should not consider this update of the economic and investment environment as analysis upon which to make investment decisions or recommendations of strategies or particular securities. Past performance is no guarantee of future results. (1414)

All trademarks, service marks and trade names referenced in this material are the property of their respective owners.